Age: 29

Occupation: Registered Nurse

Status: Engaged

Location: Marietta, Ga

Salary: $55,000

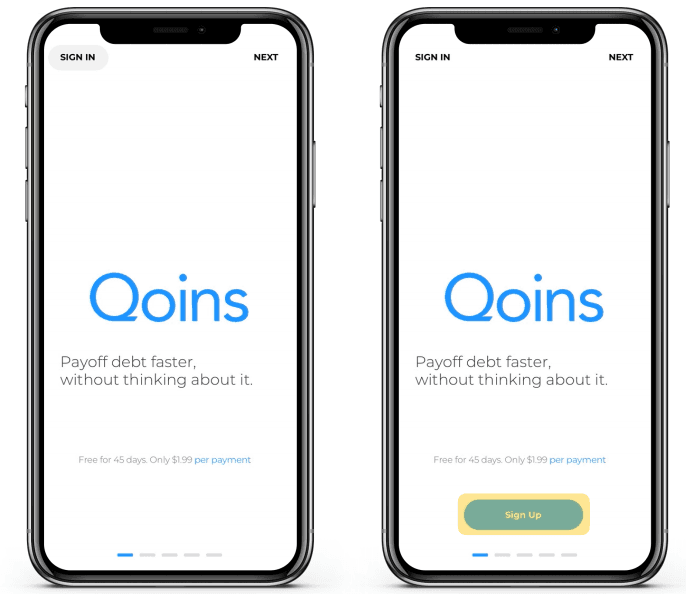

“Pay off debt faster, without thinking about it."

"Use spare change from everyday transactions to make an extra payment towards your debt, every month.”

Meet the Team

Morgan Breier

Ashton Cheeks

Briana Brock

We worked along side a client with their existing product to find out how we could improve their user’s on-boarding experience and increase their active user base, increasing revenue.

Got Debt?

The average American has between $67,000-$134,000 worth of debt.

Americans have about $3 trillion worth of interest alone, that’s about $10K per person.

While people are aware, they don’t really talk about the psychological effect massive debt has.

The emotional effects of debt include denial, stress, fear and panic, anger and depression.

But there’s a sense of relief, freedom, and accomplishment from paying off debt

What is Qoins?

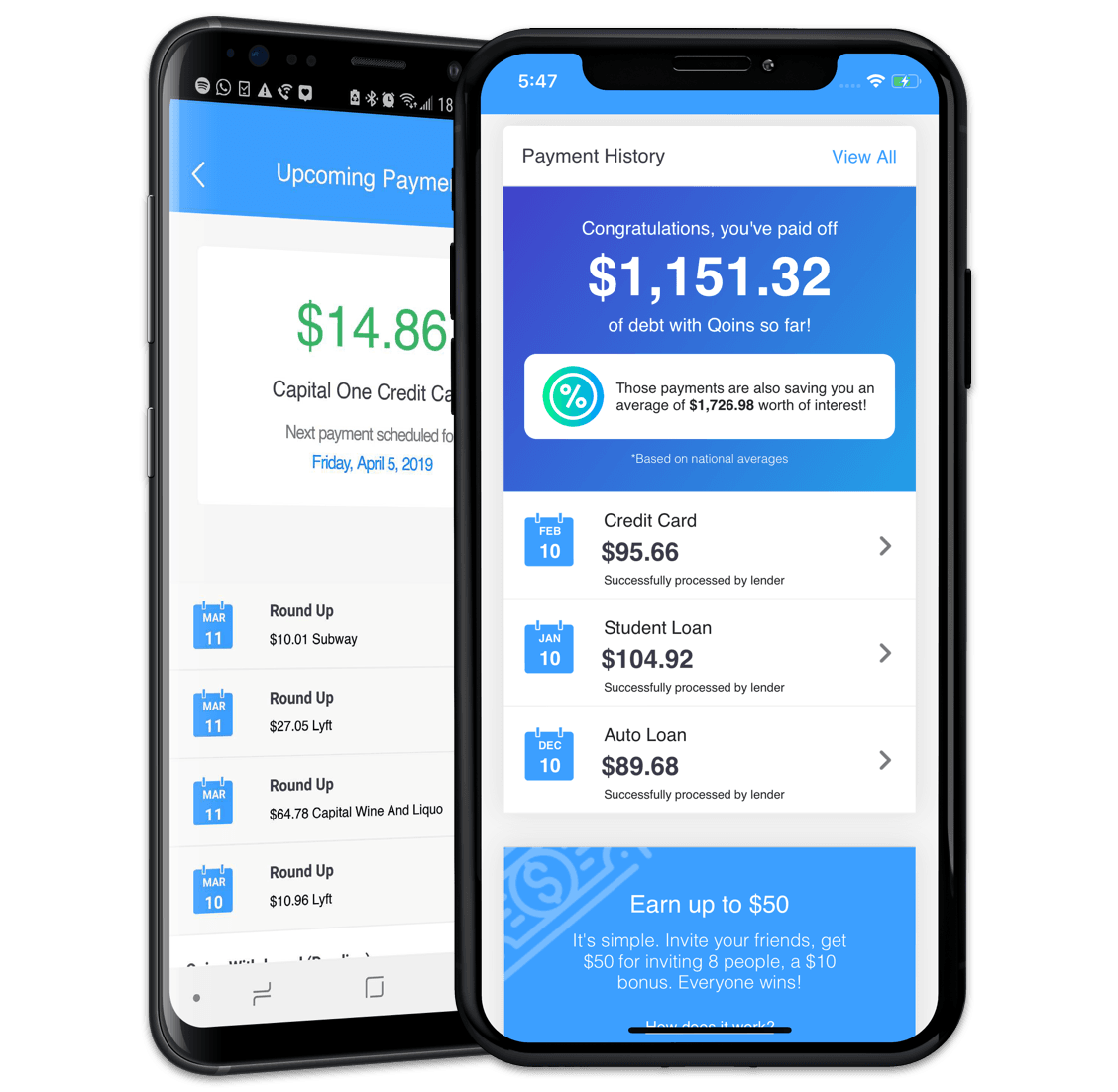

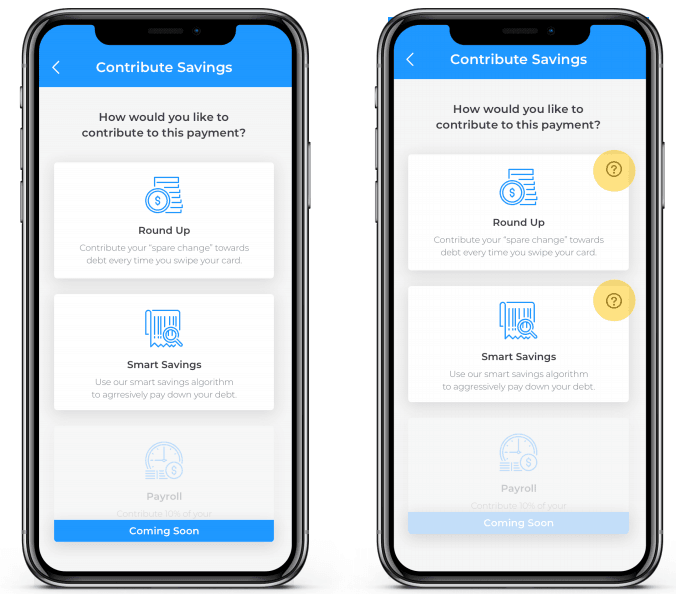

A financial management mobile app that rounds up your individual purchases and allows you to set up automatic payments to set money aside in order for you to pay off your debt faster.

How Qoins Works

Round-Up

Smart-Savings

Set Money Aside

Pay Off Debt

Qoins has over 60,000 downloads, but only 12,000 active users

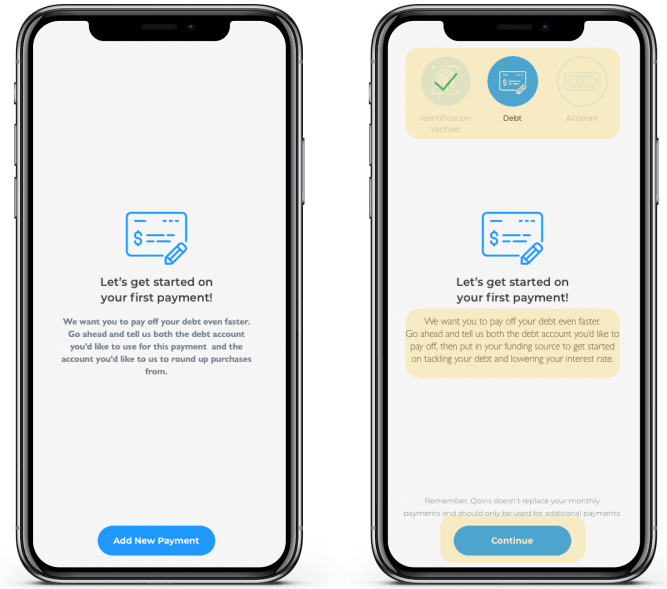

Qoins measure of success is a 3 step process:

Identification Verification

Set up your Creditor/ Lender

Set up your Funding Source

Problem

Qoins needs a way to streamline the on boarding process to increase their active users

Solution

We believe that by consolidating screens, it will lead to an easier more enjoyable experience

The Process: 2 Week Sprint

Week 1

Competitive analysis, Survey, Interviews, User Testing on Existing Product, Synthesis/Ideation

Week 2

Iterations on product for final mockup, Testing, Delivery to Client

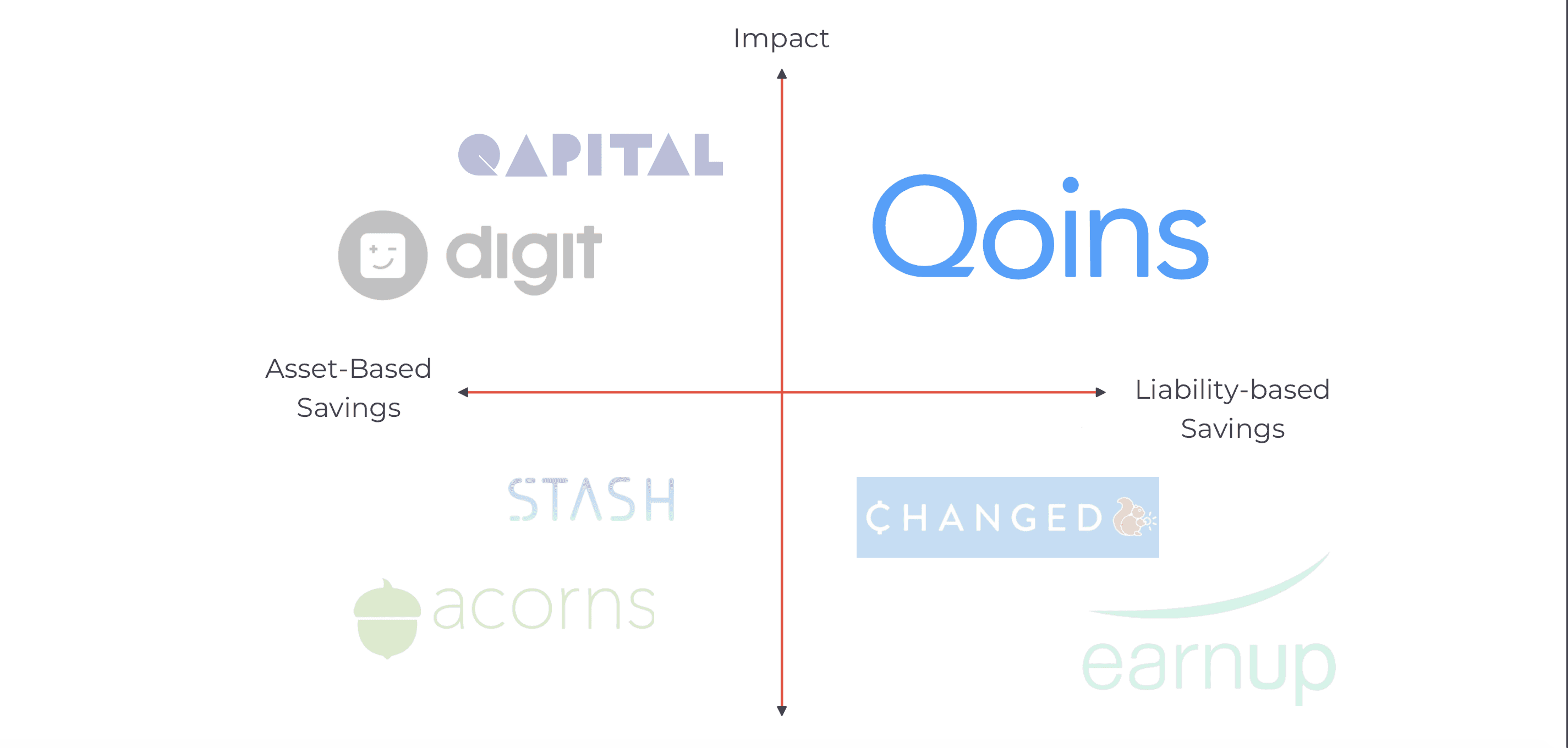

Competitive Analysis

Competitors vary with:

Monthly/various fees

Abilities and offers

Number of on-boarding screens

All having the ability to sign up after the first screen, something that Qoins does not offer

Survey

During our client meeting we requested access to their current client list to submit a survey to gauge customer interactions with the app.

We received 0 responses to the survey…

We then realized we needed access to the users who bailed on the on boarding process. While Qoins had the email addresses on those who did not complete the on boarding process, we were denied access to them.

Interviews

We interviewed 8 people with varying backgrounds, all with some form of debt

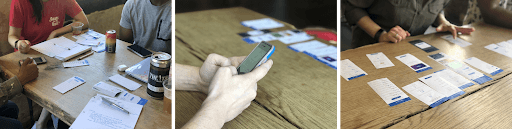

User Testing

We tested with Qoins existing app; we used paper prototypes since users must enter sensitive financial information to sign up

Usability tests proved that users became frustrated, confused, and hostile with the existing on-boarding process.

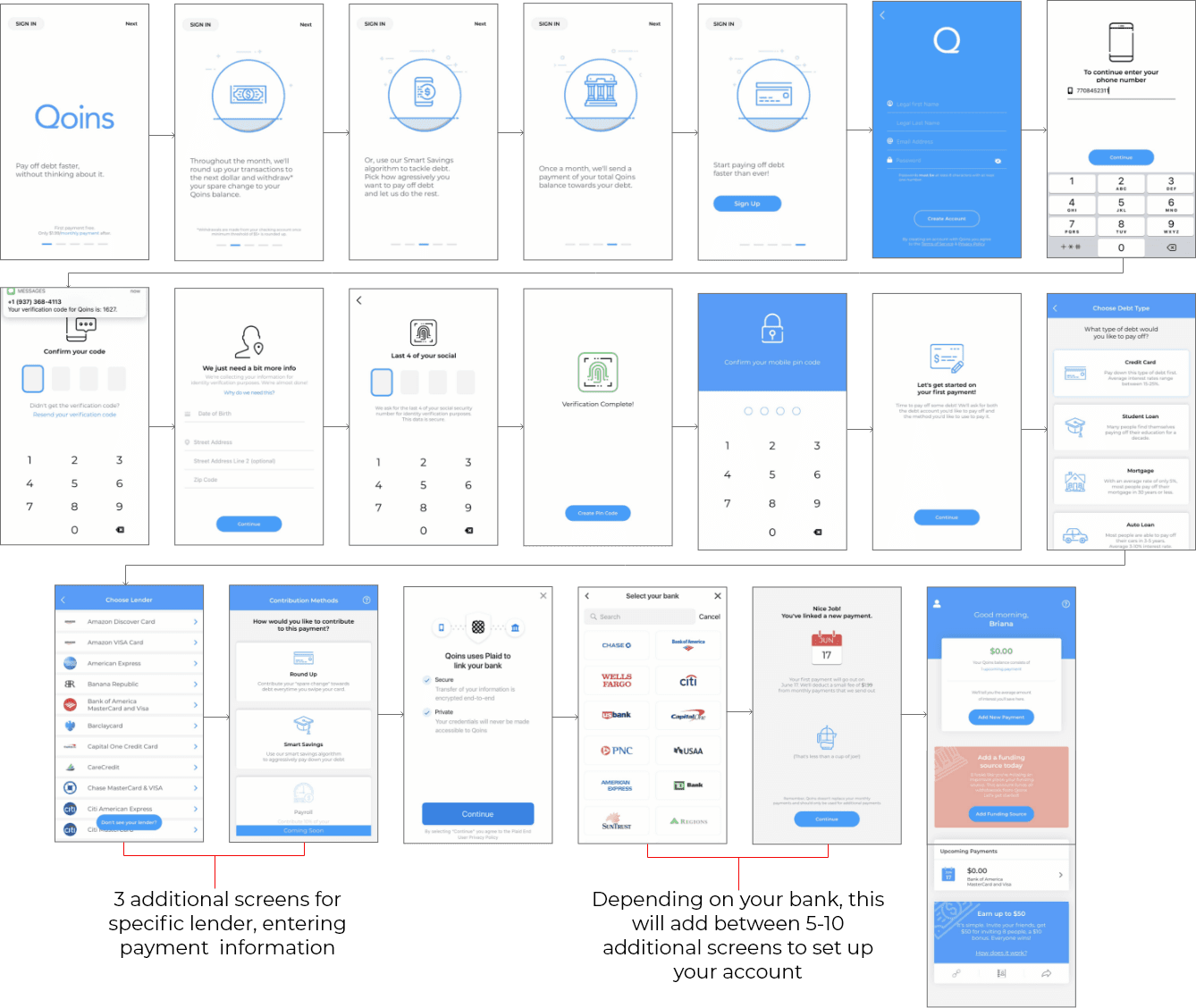

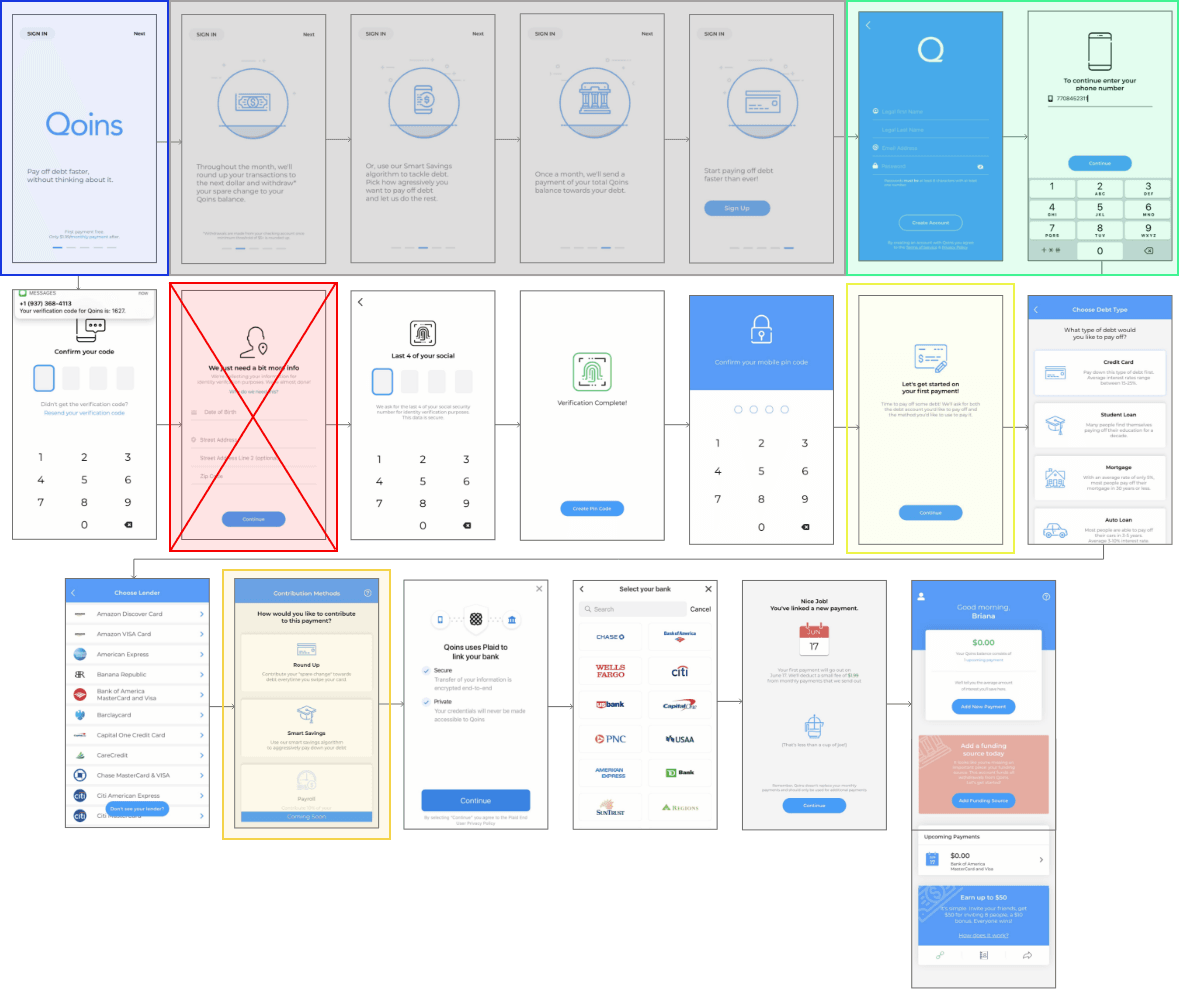

QOINS existing user flow

The on boarding process takes 20 screens to get to the homepage, with 2 separate points where adding financial lender adds 3 more screens and the funding source can add up to 10 additional screens depending on the financial institution

Synthesis

With affinity mapping, we synthesized the qualitative data gathered during usability testing

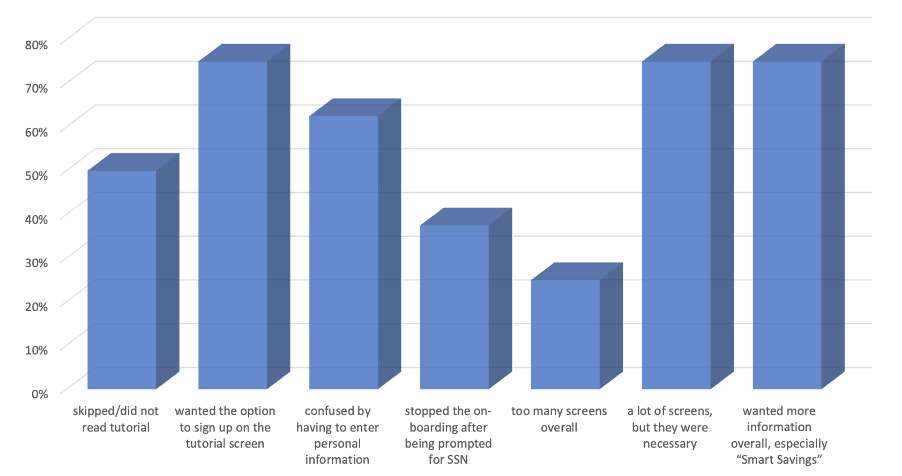

Findings

4/8- skipped/did not read tutorial

6/8- wanted the option to sign up on the tutorial screen instead of waiting until the end of tutorial

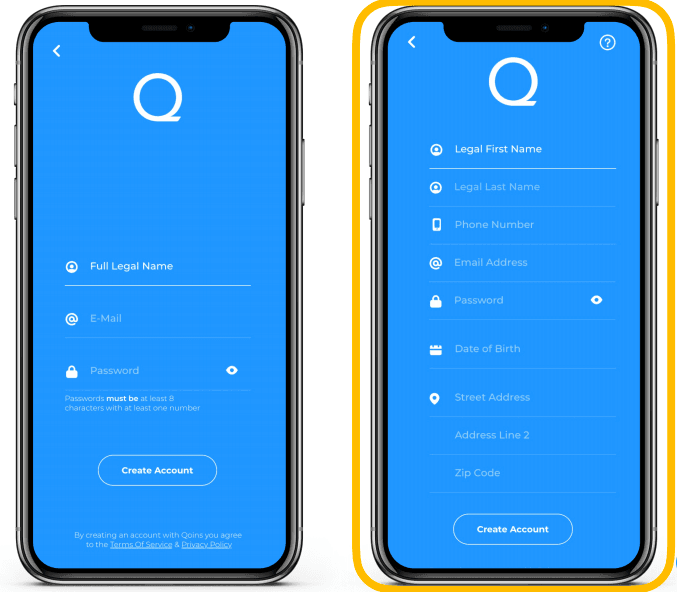

5/8- were confused by having to enter certain personal information

3/8- stopped the on-boarding after being prompted to enter their Social Security number

2/8- thought there were too many screens overall

6/8- thought there were a lot of screens, but they were necessary

6/8- wanted more information overall, especially about “Smart Savings”

One prominent issue kept getting brought up:

Trust

Users were apprehensive submitting personal financial information for an app on their phone

How do you build trust in a brand with an application you only have access to from your phone?

This is an issue we were not able to address due to time during our 2 week sprint, we will continue looking into brand trust for our next steps

Based on synthesis from interviews, Qoins target audience, and user testing, we developed our persona

Age: 29

Occupation: Registered Nurse

Status: Engaged

Location: Marietta, Ga

Salary: $55,000

Kristin Bradshaw

Kristin recently graduated from the Wellstar Program at Kennesaw State University with a Bachelor of Science in Nursing. Upon graduating, she landed a job at Emory in Midtown.

While in school, Kristin accumulated student loan debt. She and her fiancé want to get married in the next 3-5 years, and want to be debt free before they marry. After marriage, they want to buy a house together and need a good credit score for a loan.

Goals

Reduce monthly interest fees

Pay off and be debt free

Get married and buy a house

Build good credit

Pain Points

High interest rates

Minimum payments delaying paying off debt

Paying on time

Debt collectors

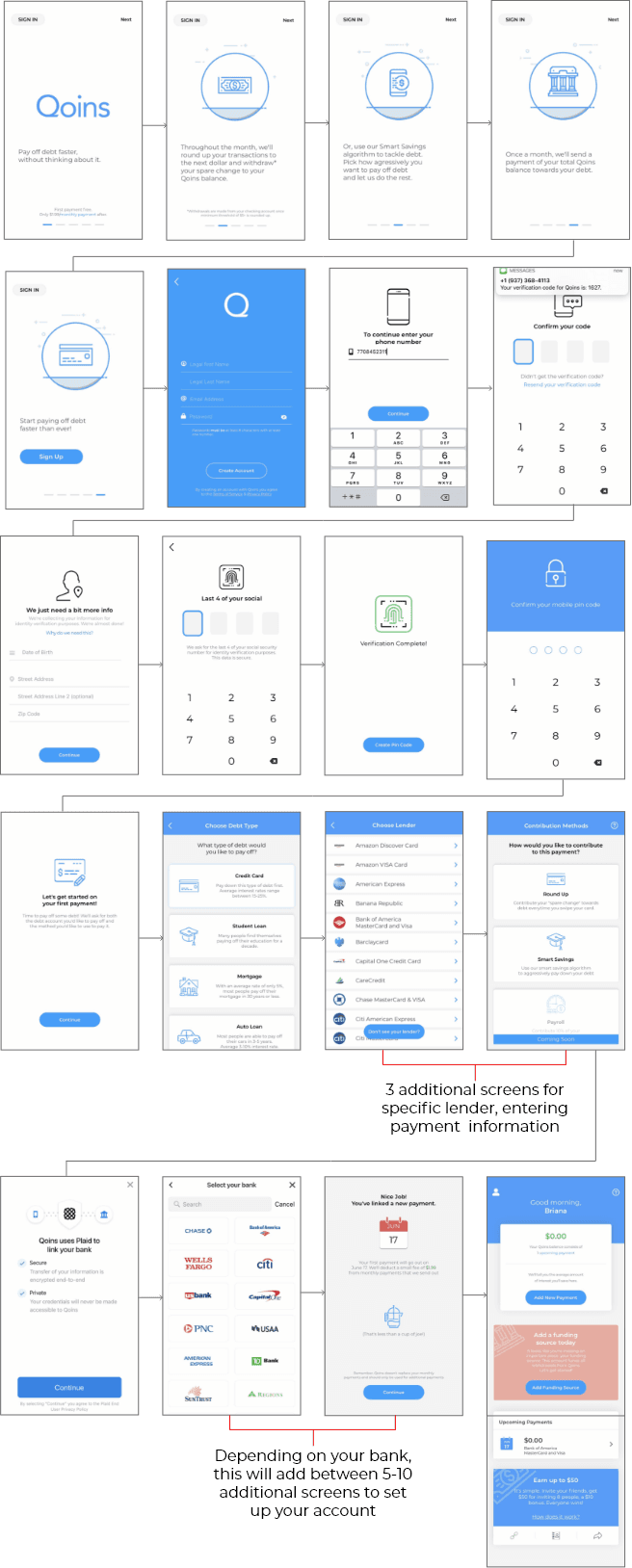

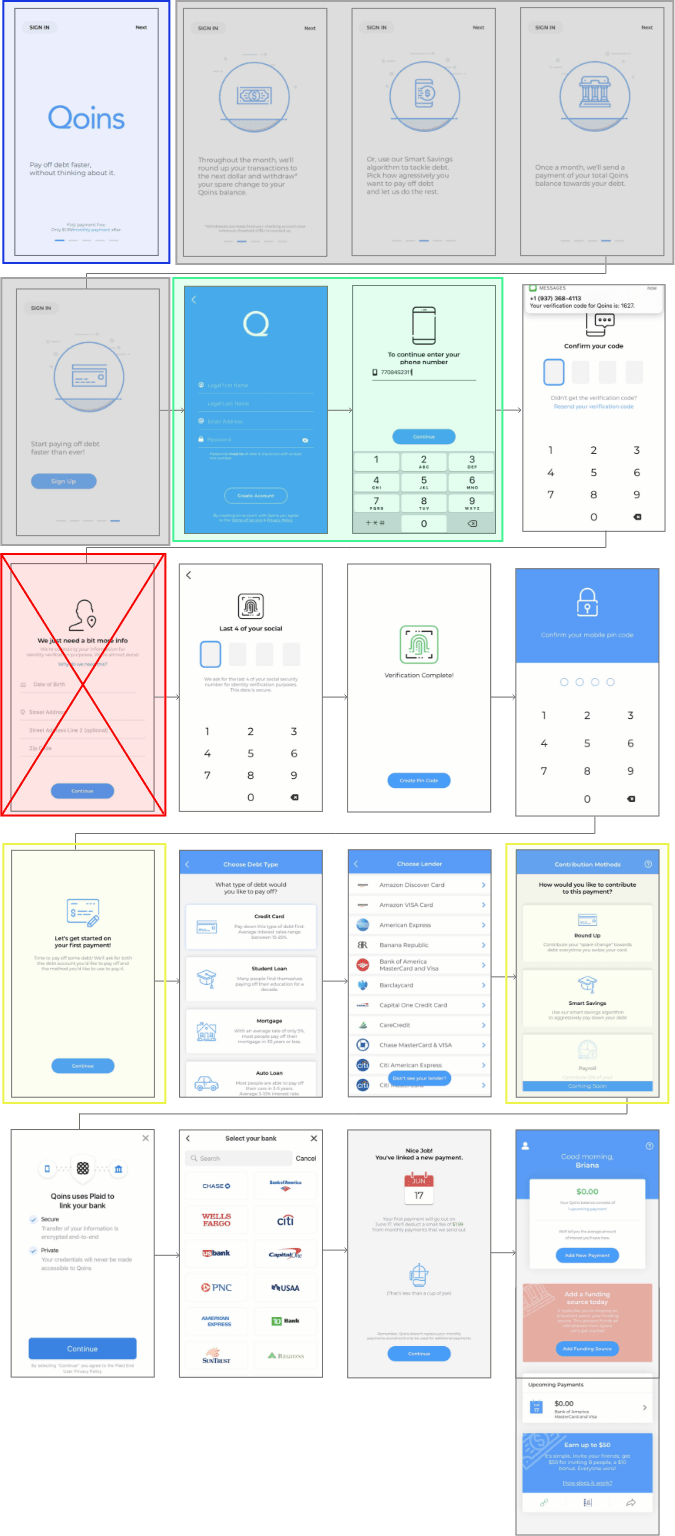

Iterations

Based on our users’ needs, we eliminated and consolidated certain screen, with optional on-boarding tutorial, and were able to streamline the on-boarding experience

Changes per screen

Next Steps

Conduct additional usability testing

Add/Subtract feature based on users’ needs

How to build trust in a brand?